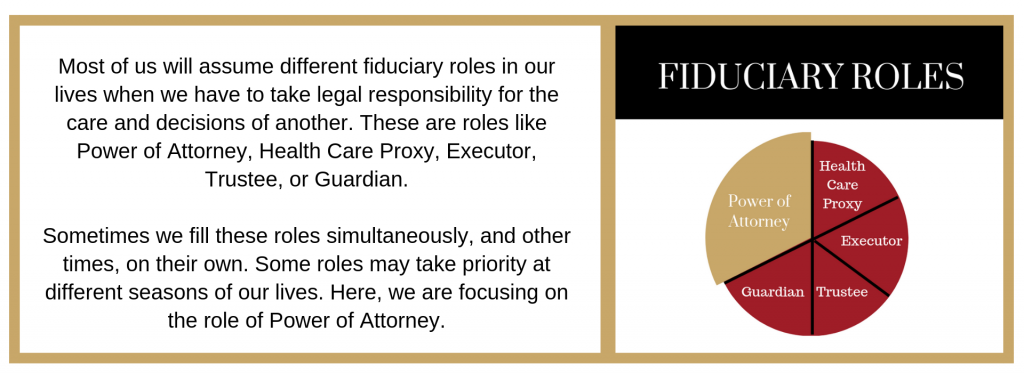

You Have Power of Attorney. Now What?

If you’ve been assigned the role of power of attorney, this information we’ve gathered will help you understand your responsibilities and the terminology involved. First, the basics: What are you signed up for? A power of attorney gives you the authority to legally act on behalf of someone else, who is known as the principal.

There are two main types of power of attorney: medical and financial/legal. This post will NOT be about the medical PoA. (We’ll deal with that when we cover the role of healthcare proxy).

The financial power of attorney gives you control over the principal’s financial and legal affairs (a) when and as directed by the principal or (b) when the principal is incapacitated (assuming the power is “durable,” as the vast majority of modern PoA documents are). The power may be limited in scope or duration if specified under the PoA document; otherwise it is of unlimited duration and authority.

The Power of Attorney Is a Powerful Role

With power of attorney, you can complete any financial or legal transaction that the principal wishes or that you decide is in the principal’s best interests if he/she is incapacitated. These can include transactions related to:

- Real or personal property

- Banking and investments

- Unincorporated business dealings and operations

- Voting business stock or LLC ownership

- Beneficiary transactions and interests related to estates and trusts

- Insurance, annuities, and retirement plan decisions on products, coverages, and investment choices

- Legal affairs, including contracts, bringing and defending claims and civil litigation

- Personal support and support of dependents

- Social security or other government program benefits if you have been named as a representative payee

- Tax matters, including preparing, signing, and filing tax returns, and dealing with revenue departments and the IRS

- Gifting

- Estate planning

- Creation or funding of trusts

To learn more about the tasks of PoA, read AgingCare.com’s article, Things You Can and Can’t Do With Power of Attorney.

Not only should you know your responsibilities as PoA holder but you should make sure you have given someone you trust power of attorney in case you are sick or incapacitated.

You should also insist that your young adult children give you power of attorney for them. After they turn 18, you no longer have authority to make health decisions and may not represent them in legal and financial matters. But they’re adults; they can refuse!

But It’s Not All-Powerful

While power of attorney is extremely useful for protecting your loved ones, it’s not a carte blanche license. For example, you cannot change the principal’s will, ignore your duty to act in the principal’s best interest, or make decisions for the principal after his or her death.

You may be met with delays when dealing with some financial institutions. They are cautious because they may be held financially liable for any wrongdoing. Financial institutions may take time to verify the legality of the PoA document with the attorney who prepared it. They may even ask you to submit a sworn written statement guaranteeing the authenticity of the PoA in an attempt to release them from liability.

Under what circumstances might you need more than power of attorney? Read AgingCare.com’s When POA Isn’t Enough: Other Forms Needed to Act on a Loved One’s Behalf.

A Day in the Life of a Power of Attorney

See what a day in the life of a power of attorney might look like in Tim’s LinkedIn article, 24 Hours as Power of Attorney Holder.

{kind=link}